The Banking Experience Summit recently convened leading bankers from three continents in Chicago to discuss the industry’s challenges and the future of banking. The two-day event drew more than 40 top institutions, ranging from large national and regional banks like JP Morgan Chase and Regions Bank to a diverse range of mid-sized institutions and credit unions.

The presenters covered a wide range of topics, including the challenges of transformation and competing with fintechs, as well as the importance of humanizing the customer experience. With the recent surge in inflation, the banking industry has emerged stronger from the pandemic and is now facing new threats from open banking and a shift to new payment platforms. We compiled five key conference insights from the various sessions that financial institutions must consider to ensure their organization and the industry remain relevant.

Image Source: Shutterstock

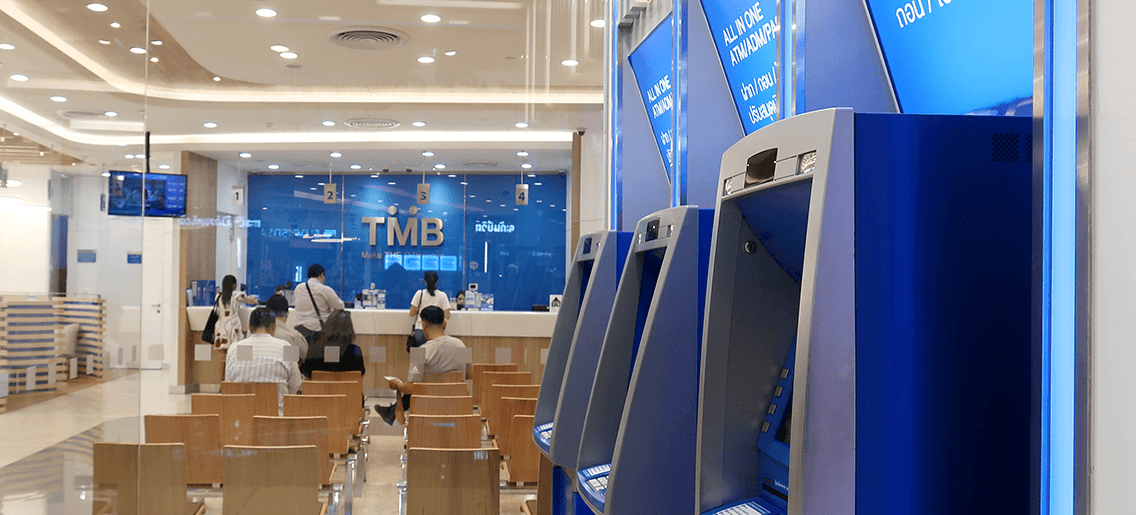

#1 – Retail Remains A Critical Channel But Needs To Evolve

The recent pandemic had a significant impact on retail banking, with many locations closing for business, forcing customers to rely on digital and ATM channels. According to our COVID-19 pandemic study on banking during the pandemic, in order to maintain a safe environment for employees and customers, banks and credit unions have introduced appointment-setting options to accommodate, which have gained popularity and are still active after the pandemic’s peak. Even after the pandemic, the branch remains an important channel for customers, with only 10% to 17% of consumers using digital as their primary banking platform. Furthermore, according to our Stealth Attrition study, which the various presenters also supported, digital-only customers have the highest attrition rate, nearly double that of branch customers.

The transition to digital banking and lower frequency of customer branch visits, combined with industry consolidation, resulted in closures and relocations as part of their network right-sizing. According to recent figures shared at the conference, over 4,000 branches have been closed since 2020, and the number is expected to rise depending on where the respective banks are on their transformation journey. Downsizing progress was also heavily influenced by the institution’s digital transformation strategy and stage, with some branches well on their way to closing. However, there was growing concern that branch closures had gone too far, with some experiencing a decline in business and significant customer attrition. Everyone agreed that the branch’s role was shifting away from transactions and toward financial services and advice. The results paint a clear picture – that retail bank branches are still the most sought-after method of banking but need to provide the right mix of digital services, financial advice and consultation, and banking.

Image Source: Shutterstock

#2 – Collaboration With Fintech Will Only Accelerate

Many bankers have noticed that the war against fintech start-ups has shifted, and many institutions have partnered with platforms to help them meet their customers’ needs faster. The difficulty that banks and credit unions face in managing their legacy operating systems is a key reason for embracing fintechs. Millennial Bank, a leading financial institution in Portugal, chose to address its legacy issues before launching new digital services and seeking a solid operating platform to help accelerate its digital transformation. Ten years after fintechs first appeared as competitors to banks, they are now viewed as collaborators to help banks accelerate their transformational programs, rather than threats. In exchange for vertical expertise on customer pain points, banks provide these organizations with credibility and access to a large pool of customers and scale.

Several speakers discussed how fintechs are assisting banks in avoiding roadblocks and allowing for rapid change. Many institutions also mentioned that the focus on creating a seamless banking experience, which is still elusive today, is through the use of APIs, which allow the integration of third-party APPs. Our research on the need for banks to move beyond traditional banking services and into digital ecosystems is just one of the many reasons why banks should collaborate to accelerate innovation. However, there was no clarity on the business and financial impact of such initiatives, as many are still in the process of validating the partnerships. The rise of fintech partnerships raises the question of how these alliances will force banks to reconsider their business and financial models.

Image Source: Shutterstock

#3 – The Race Of “Start Anywhere” Banking Has Just Begun

For most institutions, the vision of a seamless experience has been elusive because customers are forced to go through rigid onboarding and banking processes, many of which are flawed with friction. Some financial institutions have made significant progress toward closing the siloed versus seamless experience gap by flattening the organizational structure and integrating digital and physical roles under a single leader. Fidelity Bank, Northwest Bank, and Millennial Bank, for example, have restructured their organizations to centralize accountability and leadership within the bank. However, they noted that it is difficult to create a seamless experience when information about the customer is owned by a specific channel and is not widely shared across the organization.

For some organizations, the pursuit of a seamless experience must begin with automating back office processes. Many steps and approval processes are being streamlined using AI and robotics to give front-line staff the tools they need to engage with customers and provide quick approvals. However, there was widespread agreement that many of the service providers who enable automation and a seamless experience underperformed, jeopardizing the bank’s credibility. Accelerating time to market is critical, and institutions have noted that flattening the process and increasing alignment are important factors to consider.

Image Source: SLD

#4 – Humanizing CX

The race to digital transformation has prioritized technology over people, resulting in some initiatives falling short of expectations. According to our research on the state of the banking physi-digital transformation, the industry is far ahead of retail, food service, and healthcare, but it needs to focus on humanizing the overall experience. The importance of humanizing the customer experience was recognized by the presenters, who focused on employee training and motivation. A key challenge is assisting employees in embracing change as the institution transitions from transactional in-branch service to one focused on creating a greater triage between daily banking, which is now done online, and advice. The current universal banker has also produced mixed results in terms of operational efficiency and how bankers interact with customers during peak banking periods.

Presenters discussed the importance of involving employees in the development of new digital services and platforms from the start to ensure their buy-in and, more importantly, that they deliver on the brand promise. Part of the problem is that technology is moving so quickly that more effort must be put into onboarding employees. Furthermore, banks recognize the need to shift their language and communication from digital transformation to customer experience transformation. Improving the customer experience is becoming a company-wide priority, affecting all aspects of the customer and employee journey. While discussing the multitude of avenues available for enhancing customer engagement, it’s pertinent to highlight the role of technology in this realm. The adoption of a dedicated channel for communication, particularly through WhatsApp, offers a direct and personal way to connect with customers. For more information on how to implement this in your business, visit https://www.yourbusinessnumber.com/. This strategy has been shown to significantly improve the quality of customer service and interaction, setting a new standard in customer engagement.

Banks stated that any new product launch must consider the customer experience and cross-functional impact from start to finish. To identify potential friction points, the process begins with understanding the various customer personas and their banking journeys. The approach must also take employees into account, assisting them through coaching on the role and value of digital, which translates into digital confidence for banking customers. Finally, putting bankers in their customers’ shoes will help ensure that the experience is tailored to their specific needs and priorities.

Image Source: Shutterstock

#5 – Corporate Silos Are The True Transformation Enemy

Bankers identified organizational silos as a major barrier to providing better customer experiences. Leading banks are combining their customer and marketing views at the enterprise level, shifting responsibility away from individual business units to ensure a more holistic approach. Most bankers agreed that in order to become truly seamless, the organization must focus on breaking down inter-company barriers, flattening processes, and increasing internal alignment. Many of the considerations that organizations must consider during the transformational process are highlighted in our customer journey mapping blog.

Banks are considering new ways to track the overall customer experience in addition to creating a more cohesive organization with a single view of the customer across all products. SLD’s Measuring What Matters study identifies the gap that financial institutions must bridge in order to provide an immersive customer experience. Some institutions, for example, are better at leveraging their data to understand the gaps in the customer experience. Others, on the other hand, have implemented sentiment analysis as an assisted channel to better respond to customer inquiries. Another effective strategy for breaking down organizational silos is to foster a more inclusive culture in which cross-functional teams crowdsource ideas. To avoid experience gaps, any new product launched should consider the entire end-to-end experience across cross-functional departments.Employee engagement, not employee happiness, is what will drive growth, according to presenters. Therefore, measurements need to evaluate the various types of employment and how they impact the overall customer value.

MOVING FORWARD

In-person conferences provide an excellent platform for learning and sharing ideas, while also allowing the industry to recognize that most institutions, regardless of size, face similar challenges. Financial institutions are on the verge of change, driven by both external forces, some of which are beyond their control, and internal dynamics that limit the organization’s ability to provide a seamless customer experience. Nonetheless, the conference concluded that many institutions are on the right track in terms of engaging their customers in new and meaningful ways.