The future of payment systems has been evolving as technology continues to make its mark on the payments landscape. Finance and retail have long been inextricably linked, and with customers obsessing over the latest technology, payment systems have had to keep up. In this dynamic environment, businesses are increasingly exploring innovative solutions to streamline transactions, and one notable option gaining traction is the integration of Nav Credit Cards into their financial strategies. This forward-thinking approach not only aligns with the digital era but also offers businesses enhanced flexibility and efficiency in managing their financial transactions. Get the best rates with merchant account comparison. This blog will look at the new, innovative payment systems that are being implemented around the world to satisfy tech-savvy customers.

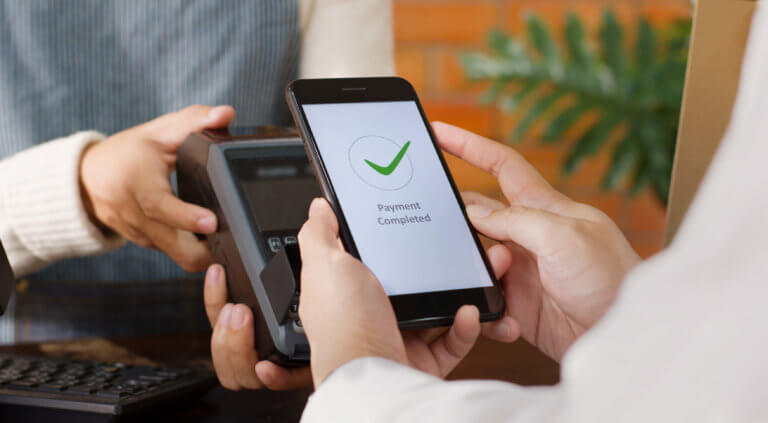

1 – Mobile Wallets

As companies continue to implement new ways to accept mobile wallet cards, the use of mobile wallets has grown in popularity. According to PWC, mobile wallet purchases will skyrocket over the next decade. They estimate that nearly two trillion transactions will be made using mobile wallets by 2030. Because of its ease of use and touchless design, it has become one of the most popular forms of payment for many people, which has been accelerated by the pandemic.

Mobile wallets include a variety of features that help to protect the user. During the pandemic, when the risk of contracting the virus was high, this was deemed to be much safer as an entirely cashless and touchless system. Another advantage of mobile wallets is the encryption services they provide. Rather than inserting a card that stores your information, mobile wallets transmit a Device Account Number rather than card data (DAN). If someone obtains this number, it will be worthless to them in comparison to a credit card number. With the rise of wearable technology, smartwatches can also make contactless payments more convenient by using this DAN number.

Image Source: Shutterstock

2 – SMS

Countries all over the world are beginning to use mobile phones in novel ways, including how payments are made. While digital wallets are one aspect, businesses are beginning to use every teenager’s favorite payment method – text messaging.

In some parts of France, simply texting “bus” followed by the route number to a designated phone number can get an individual a bus ticket in seconds rather than purchasing paper copies, saving time and becoming more environmentally friendly in the process. The payment is then applied to the user’s cellular bill and will appear on their monthly statement. The ability to purchase bus tickets in seconds on a device that most people carry with them at all times is a convenient use of technology that can be expanded to sectors other than public transportation.

3 – QR Codes

Some may believe that QR codes were a passing fad that peaked in popularity in the mid-2000s, but this is not the case. QR codes are more popular than ever, but not in the United States. As mobile wallets are the preferred method of currency transfer in Asia, QR codes are a dominant method of information transfer. Most Chinese people never carry cash or credit cards as mobile wallets are the most popular, with over 800 million users.

QR codes have been adopted for almost every payment need in China, from purchasing a beverage at a local shop to purchasing larger items such as electronics. The QR code’s greatest strength is its adaptability, and its incorporation into North American payment systems would be a welcome addition as the region’s reliance on mobile wallets grows. You may want to try these independent financial advisor coaching programs to learn more about financial planning topics that you’re not as familiar with.

Image Source: Weixin

4 – Crypto/Digital Bank Currency

The rise of blockchain technology has become a divisive topic, with differing viewpoints ranging from elaborate Ponzi schemes to the next form of global currency. Whatever one’s beliefs, digital assets have grown in popularity over the last decade, both with the general public and as a payment method. Bitcoin and other cryptocurrencies enable real time payments with no transfer fees, and has become a viable payment method. (Source: bitcoinkeskus.com)

Chipotle has made headlines for being one of the first restaurants in the USA to accept cryptocurrency payments, thanks to its partnership with the digital asset payment platform Flexa. Customers can walk into a Chipotle and pay using the Flexa app, which is linked to their digital wallets, thanks to the partnership. Chipotle now accepts 99 different digital currencies that have been seamlessly integrated into their business model because Flexa integrates into existing payment technology.

5 – Biometric Authentication

Biometric authentication has progressed from sci-fi fantasy to a reality in our daily lives. To unlock the phone, log in to apps, or approve mobile payments, the latest smartphones require facial recognition software. This technological evolution, with the help of an it support, has seamlessly integrated advanced security features into our everyday digital interactions.

With WeChat Pay and Alipay dominating the Chinese financial landscape, these integrations enable payment or access to bank accounts via facial recognition. All the user has to do is place the products they want to buy on the scanner and place their face within the circle on the screen, allowing the reader to scan their face and deduct the funds from their linked account.

Amazon recently debuted Amazon ONE, a similar payment system that consists of a reader attached to a payment machine. All the customer has to do is wave their hand over the reader, and the reader will identify the customer and deduct funds from their linked account using the customer’s linked palmprint and unique vein configuration.

Image Source: Amazon

6 – Voice Command

It was only a matter of time before “Hey Google” and “Hey Alexa” made their way into the financial system, given their integration into everyday life for household tasks. For voice command-activated payments, Amazon has already partnered with over 11,000 Exxon and Mobil gas stations across the United States. At select locations, the user simply says, “Alexa, pay for my gas,” and the payment is deducted from their AmazonPay account. Payment can even be made using the car itself with its Echo Auto product.

The Future of Payment Systems

As consumers’ preferences shift toward more technologically advanced solutions, financial systems and businesses will strive to adapt to the latest technology. What seemed unattainable only a few years ago is now a reality, from paying with facial recognition to purchasing a midnight burrito with Dogecoin. The best way to prepare for such a change is to use strategic foresight and consider every possible way that such a shift in payment structures may affect your business and the customer experience. The question is, is your company prepared?