How do you measure experience? This is the question SLD’s recent study aims to answer. Justifying the business case for transformation through return-on-investment metrics has been a critical challenge for financial institutions on the path to “physi-digital” experiences.

However, some factors are more easily measured than others. The emphasis on supporting business decisions with fact-based, traditional performance metrics is both logical and risky: the downside of data-driven initiatives is some factors cannot be summed up nicely with numbers.

The need to account for human-centered factors was seen as highly important by the financial executive respondents in our study; however, measuring these with a substantial degree of accuracy is not currently well understood. This conundrum is the basis of our research. The term Return on Experience (ROX), first coined by PwC, is emerging as a systematic way of measuring success. However, the use of ROX measurement is new and the level of understanding is limited.

Therefore, SLD launched a survey to determine the level of awareness, understanding, and usage of ROX metrics amongst executives of financial institutions. In addition, the study explored the importance of evaluating customer experience (CX) to determine potential perceptual gaps between institutions and the people they serve. Lastly, we explored the role branch renovations play as part of the customer experience in driving customer engagement and sales growth.

Hypothesis

The main hypothesis of our research was that although customer experience is increasingly seen as a key driver of differentiation and loyalty, financial institutions do not yet have adequate ways to properly evaluate and monitor experience factors. Some of the finer points we wanted to explore are:

- Is there a relationship between the appreciation of tracking ROX and bank performance?

- Is a bias towards ROI metrics impeding the adoption of ROX metrics?

- Is there a gap between consumers’ and banks’ evaluation of experience? How important do they perceive the emotional factors of the brand experience to be?

- What is the impact of branch transformations on growth?

- Do branch transformations have an impact for consumers who are banking primarily online?

READ THE FULL REPORT

Take a deep dive into how financial institutions can successfully embrace digital transformation.

DOWNLOAD NOW

Research Goals

The study objectives consisted of helping senior leaders and managers to:

- Understand the most commonly used approaches towards transformational programs.

- Determine the depth and reach of programs and who is leading the charge.

- Identify the level of internal alignment on the direction and strategies.

- Identify areas of vulnerability and opportunities.

About the Study

Executives were asked a series of questions regarding their approach towards their transformational program. In addition, the study explored 48 different initiatives beyond digital transformation and its reach and integration across the organization.

Research was conducted during May 2021 as part of an online study. The survey sample reflects senior management members from the CEO and C-Suite to mid-level managers and directors across all three industries.

EIGHT HIGH-LEVEL INSIGHTS

In reviewing the combined responses between banking executives and consumers, we identified eight significant insights on the branch’s role, the importance and relevance of ROX measurements, and considerations driving greater visitation and brand loyalty.

#1: Branch network remains an important channel

Although a significant percentage of transactions have shifted to online, the physical branch remains a vital channel for banking consumers. 29 percent of consumers and 24 percent of banking executives indicated their primary transactions are done in physical locations.

More important to note, more than 50 percent of customers frequent their primary branch at least once a month, while only 14 percent indicated they never visit a physical branch. 29 percent of consumers and 24 percent of banking executives indicated their primary transactions are done in physical locations.

14%

Only 14 percent never visit a branch.

60%

50%

29%

Percent of consumers and 24 percent of banking executives indicated their primary transactions are done in physical locations.

Image Source: Shutterstock

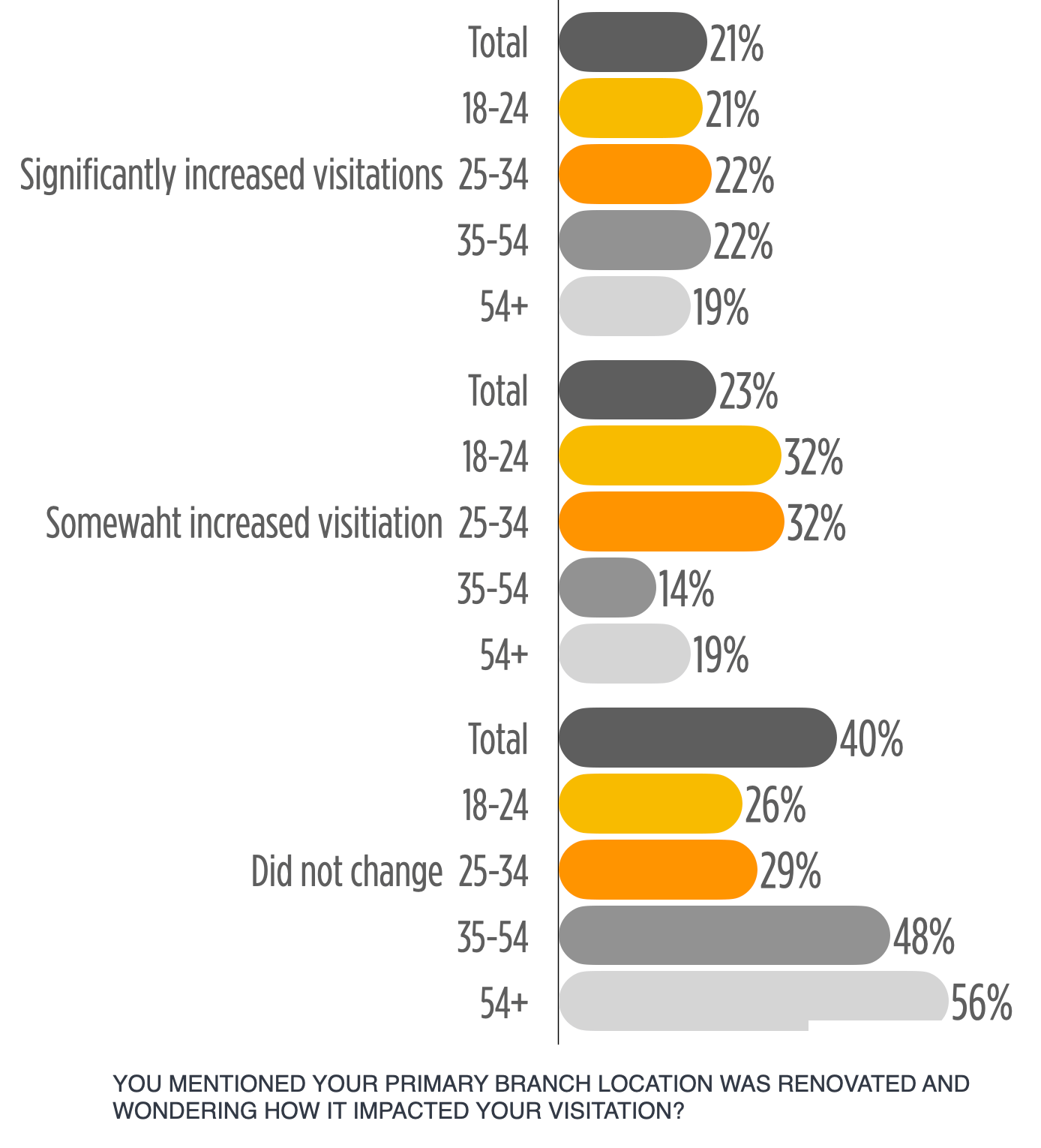

#2: Renovated branches drive 20X times visitation and growth

Customers whose bank was renovated indicated this increased their visits significantly and drove them to purchase more services and products. The 24 to 35 age group was impacted the most, with 56 percent indicating their visits increased somewhat to significantly.

More importantly, renovations drive increased revenue, with this age group indicating they had increased investments in financial products by 36 percent. On the flip side, locations with non-renovated branches had the lowest incidence of visits and lowest sales’ growth.

Image Source: Shutterstock

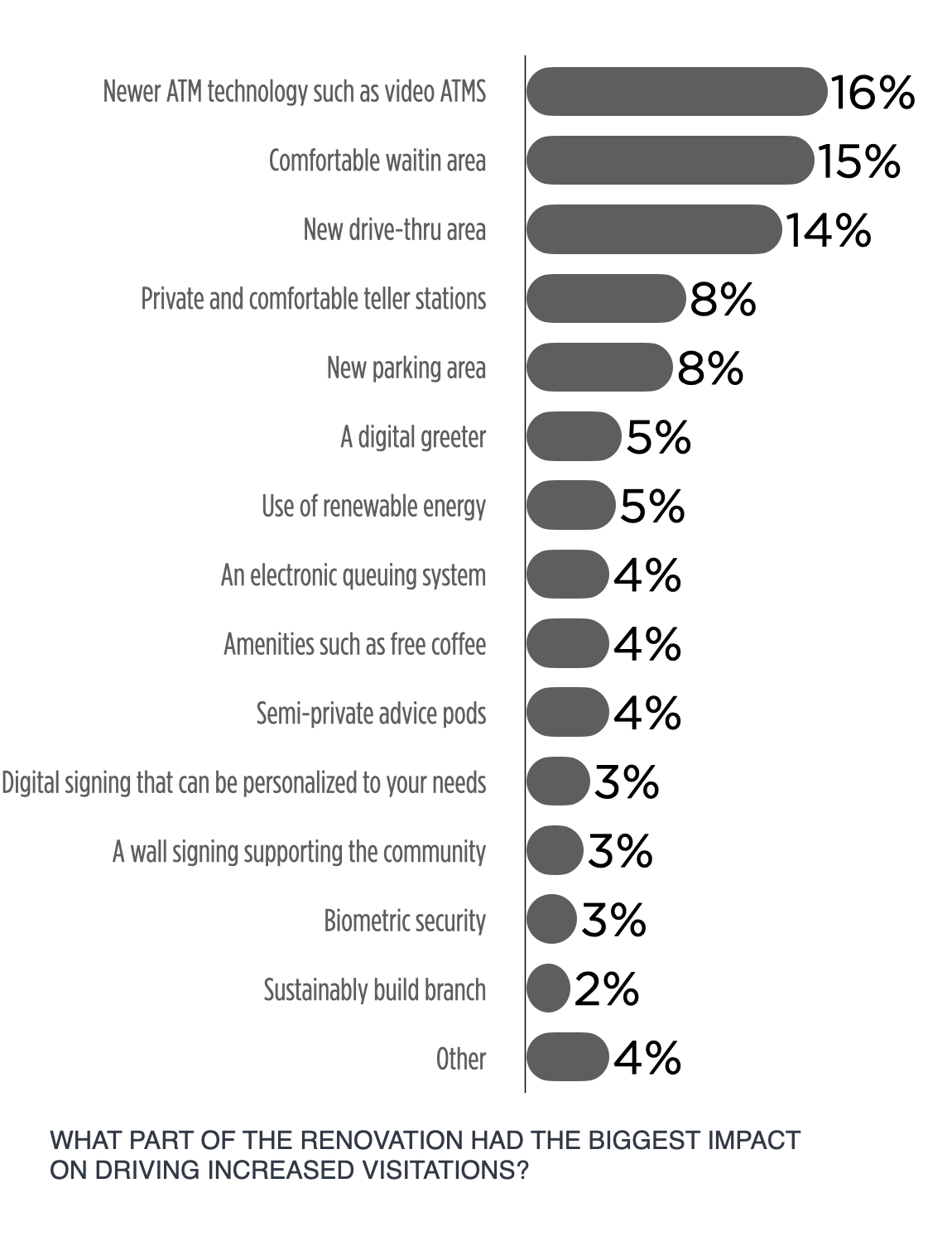

#3: ATM and drive-thru need to be considered more thoughtfully

Customers who indicated their renovated branch drove them to visit more often cited access to new ATMs, the drive-thru and more comfortable waiting and teller areas as the fundamental reasons. However, when asked what the most significant issue to resolve is, the majority mentioned the 24-hour ATM area.

ATM and drive-thru areas have often been ignored when it comes to experience, with an emphasis on speed as the primary purpose for using this channel. However, the survey results suggest there is a need to consider these short trips through the lens of experience more carefully.

Image Source: Shutterstock

#4: Big banks are tracking ROX more often than smaller banks

The study identified 52 percent of financial institutions do track some ROX metrics, led by organizations with 500 to 5000 employees. The main reasons cited are:

- impacts profitability

- provides greater performance accuracy

- allows for better planning

- tracks customers’ long-term value.

62%

Of large financial institutions track some measures of ROX

42%

Of smaller financial institutions track some measures of ROX

38%

Of no growth financial institutions track some measures of ROX

Image Source: Shutterstock

#5: Many banks do not monitor the pre-purchase stage

In addition, when asked what part of the customer journey executives track for in-branch transactions and sales, many institutions do not monitor the pre-purchase stage while the majority of the focus is around the purchase and retain steps, with the latter having the most significant level of being fully deployed.

Not surprisingly, the online transaction also mirrors the same approach to in-branch transactions. In addition, most leading, lagging and progress indicators are tracked either once a week or month. However, a great customer experience impacts all three stages of the banking journey.

- ATTRACT

- TRANSACT

- RETAIN

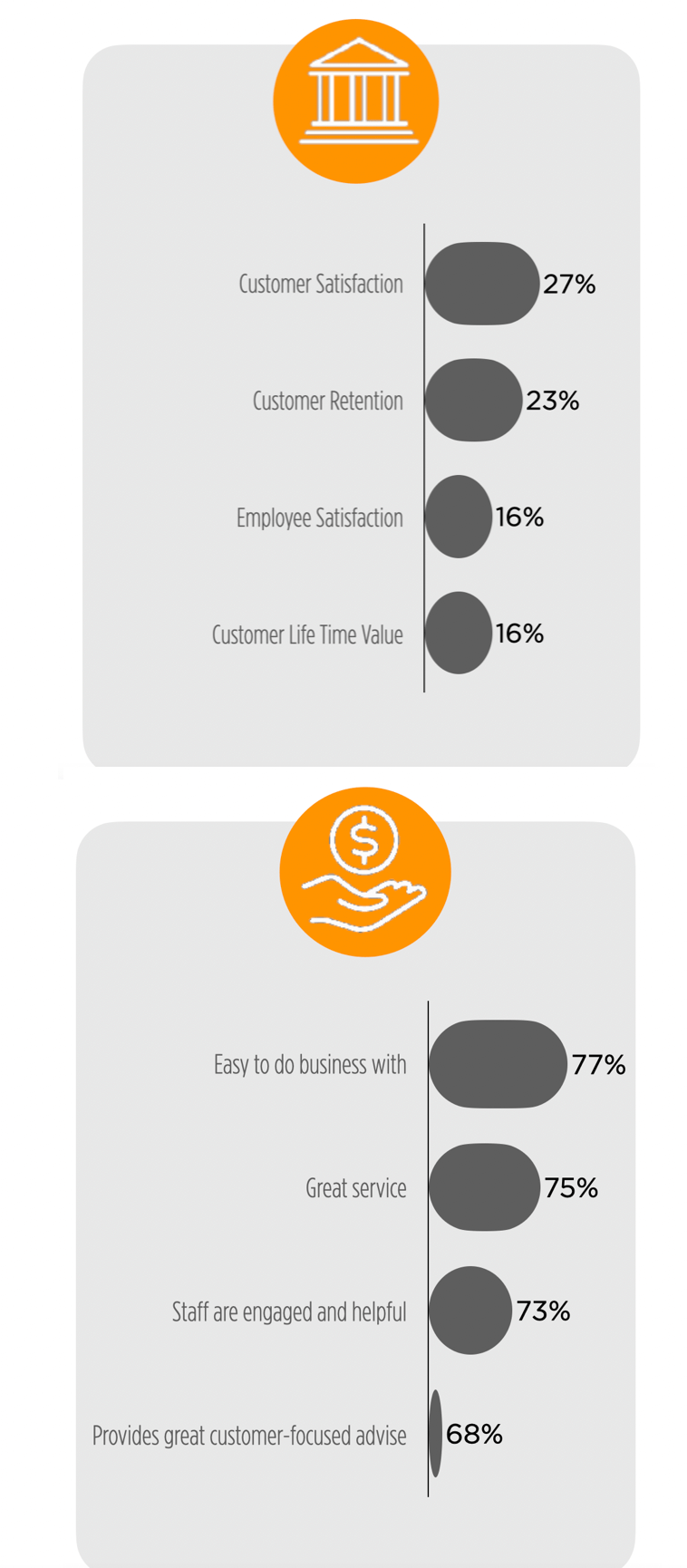

WHERE CUSTOMERS MEASURE A BANKING EXPERIENCE

Customers evaluate a great banking experience through the entire banking experience, from when they are making financial decisions to how issues are resolved. Factors such as easy to do business, great customer service to providing great customer advice ranked high in the study in defining the ideal experience.

36%

Visit a renovated branch more often.

23%

A high level of trust defines the ultimate customer experience.

WHERE BANKS MONITOR CUSTOMER EXPERIENCES

Banks put greater importance on tracking transact and retain stages of the customer experience with metrics focused on lagging indicators such as customer satisfaction, customer retention, and employee satisfaction.

24%

Pre-purchase tracking is fully deployed.

30%

Pre-purchase tracking is in the planning stages.

WHERE CUSTOMERS MEASURE A BANKING EXPERIENCE

40%

Of customers more likely to purchase more products.

20%

Of customers willing to spend significantly more with a bank great customer experience.

WHERE BANKS MONITOR CUSTOMER EXPERIENCES

33%

Transaction tracking is fully deployed.

21%

Transaction tracking is in the planning stage.

A GREAT CUSTOMER BANKING EXPERIENCE

44%

Of customers become their preferred bank.

42%

Tell a friend and family about their great customer experience.

WHERE BANKS MONITOR CUSTOMER EXPERIENCES

36%

Post-purchase measurement tracking is fully deployed.

22%

Post-purchase tracking is in a planning state.

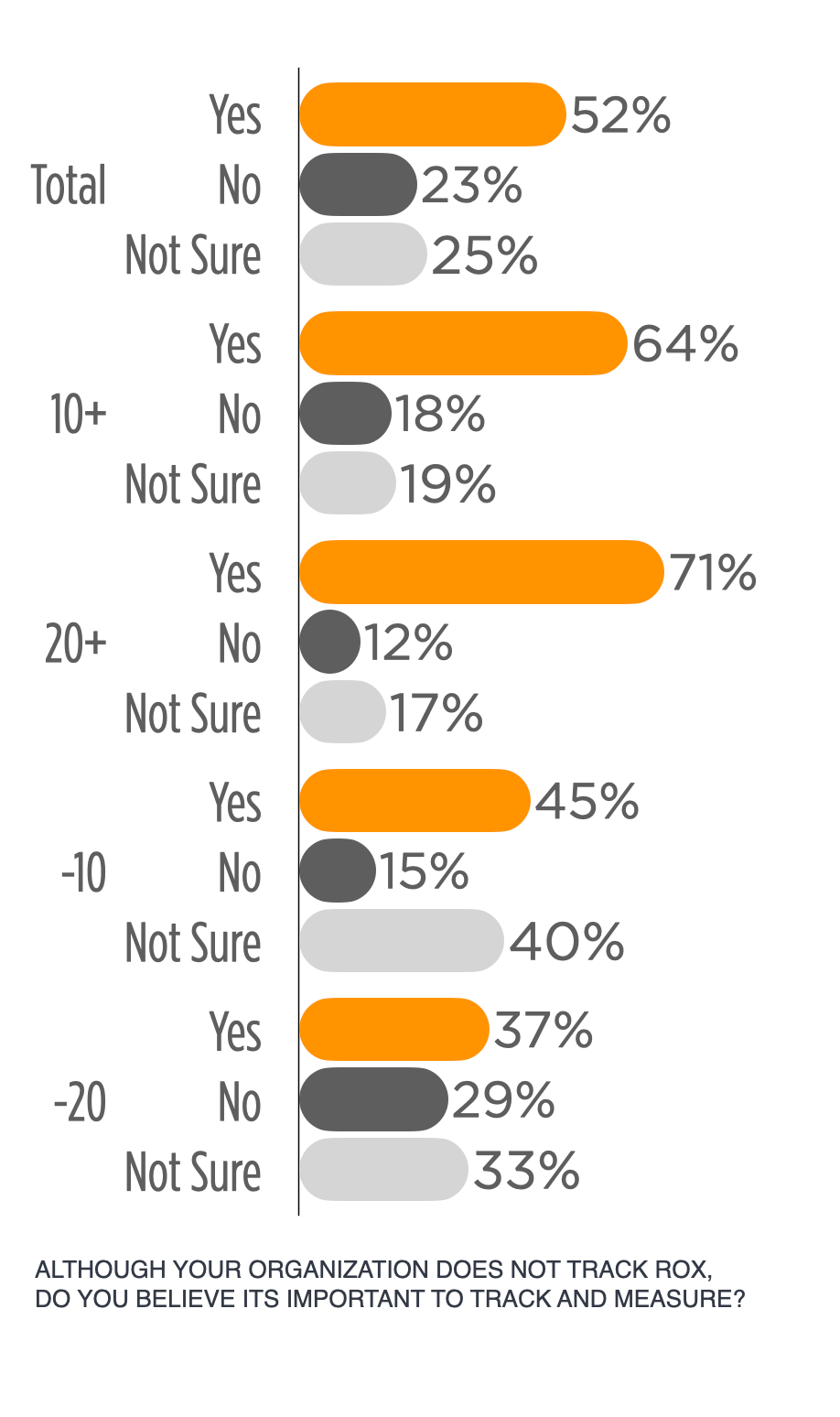

#6: ROX focus is connected to growth

In our survey, we saw a strong correlation between the measurement and understanding of ROX and growth. Institutions that grew ten percent or higher in the past three years had more transactions at physical locations and were also tracking ROX at a higher level (67% vs 52%).

These metrics include social and environmental impact, company culture, employee engagement and sales metrics, and tended to rate customer satisfaction scoring as more important compared to the overall sample.

In contrast, banks that saw a 10 percent or greater decline in business in the past three years are also the least likely to track ROX or track fewer factors. This segment relied less on the branch network, view operational metrics as more important than other factors.

Image Source: Shutterstock

#7: Banks want loyalty but are not measuring what customers value most

The customer view versus the bank executive view reveals a significant gap in what a successful banking experience means. For banks, measurements are focused on profits, not the consumer. However, customer-centricity is one of the key areas of opportunity for banks.

For example, customers indicate banks are not meeting their expectations for financial advice – and yet assessment of advice is not a top metric according to executives. For bankers, tracking ROX is financially driven, with impact on profitability being their most significant reason to track these metrics.

For consumers, the competitive price was not ranked as a key driver: ease of doing business, excellent customer service, the staff is engaged and helpful ranked the highest. In reviewing the results, it’s clear most banks are not focused on delivering the experience customers actually want.

This lack of emphasis on humanistic metrics is very concerning as customers link ease of banking, speed of transaction, level of expertise, level of attentiveness to their needs and understanding customers’ needs as critical in rating their overall experience.

Image Source: Shutterstock

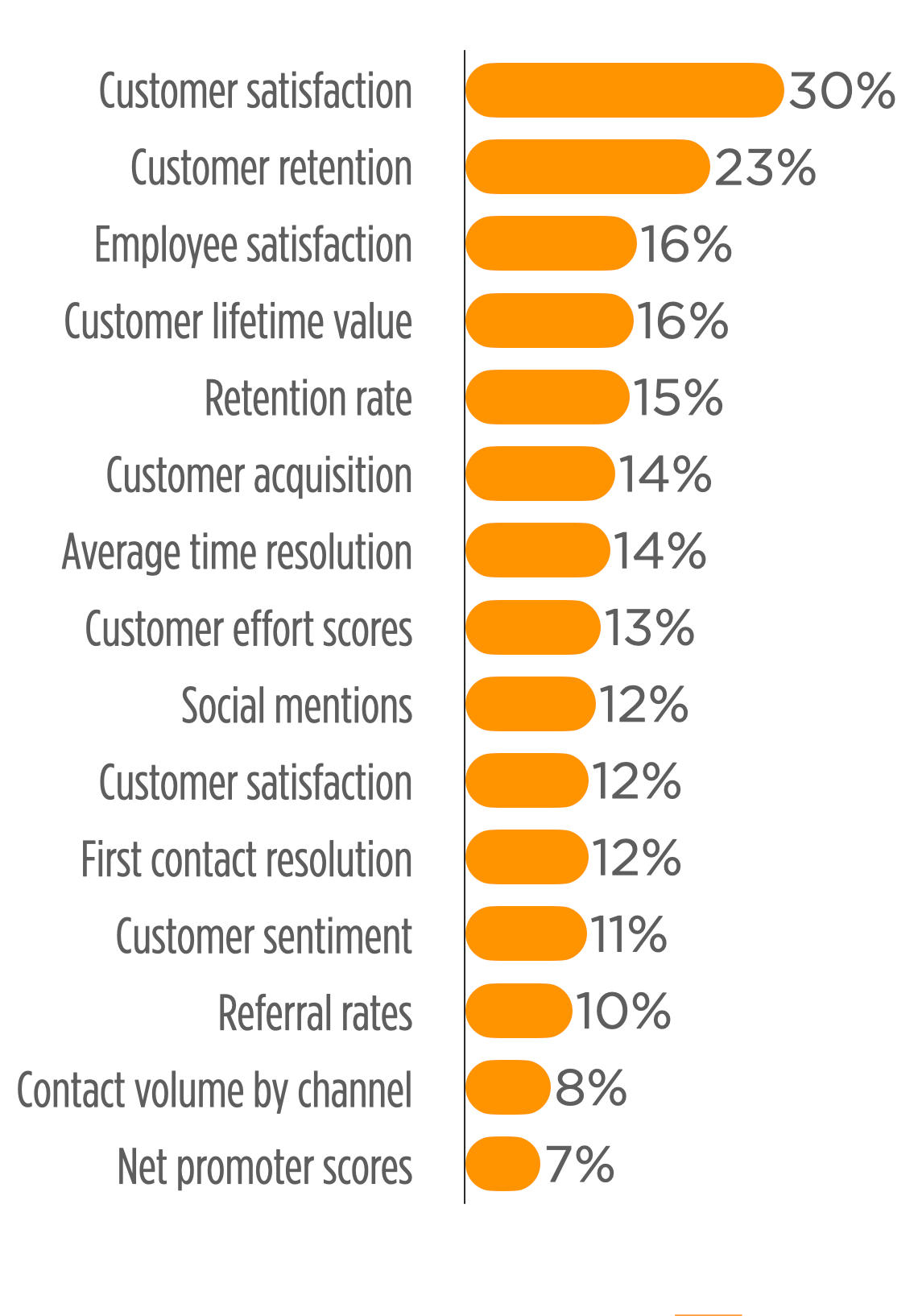

#8: Measuring how customers and employees feel are the gateways to integrating ROX measurements

Although the gap between how institutions and customers evaluate experience is concerning, banking executives do identify the use of customer sentiment and emotion scores, employee engagement, retention and effort scores as ROX metrics that could be feasibility integrated into their tracking.

Factors such as net promoter scores, customer lifetime value, and conflict resolution scored significantly lower, indicating that financial institutions still lack a strong understanding of the value of ROX. Tracking these new metrics is critical as customers define a “WOW experience” as exceeding their service expectation, resulting in higher NPS scores, and the purchase of more products and services in the future.

Image Source: Shutterstock

SIX STRATEGIC OPPORTUNITIES

Image Source: Shutterstock

ACCELERATE BRANCH TRANSFORMATION

Renovated branches have 20 times more visits and higher sales growth, with the most significant influence on the 25 to 34 age group. This is a key demographic who are in a wealth development stage and rely on their financial institutions for expertise and service. However, the impact of branch transformation does decline over time, meaning branch transformation needs to be regularly revisited. Design programs need to consider this an ongoing need.

Image Source: Shutterstock

CONVENIENCE-FOCUSED CHANNELS ALSO NEED TO DELIVER ON EXPERIENCE

Banks have spent years focusing on convenience – and yet, many services designed to be expedient, such as ATMs and apps, do not deliver meaningful experiences, leaving customers dissatisfied. Convenience is key but it needs to be connected seamlessly to experiential factors, such as service, interpersonal communication with staff and customer-centric design.

Image Source: Shutterstock

EXPAND CURRENT ROX METRICS TO INCLUDE MORE CUSTOMER-FOCUSED FACTORS

Banks are focused on outcome metrics such as financial results, sales and performance accuracy instead of monitoring overall experience factors such as customer friction points, employee engagement and company culture, of which all of these have a significant impact on future business outcomes.

Image Source: Shutterstock

ACCESS TO EXPERTISE IS A CRITICAL AREA OF OPPORTUNITY

Customers want to feel confident in the level of expertise being offered – something currently ranked very low. Rethinking how banks offer advice from a customer-centric rather than a sales-centric perspective is key to creating consumer confidence in the bank and in their own financial future.

Image Source: Shutterstock

ACCELERATE THE USE OF BEST-IN-CLASS RESEARCH TOOL

Banks currently rely heavily on quantitative research and third-party industry reports to understand the customer perspective. While these resources can be helpful in providing a starting point, these studies are based on retrospective self-reporting rather than real-life, in-the-moment experiences and emerging needs. Institutions need to increase their use of tools such as ethnography, behavioral insights, neuroscience, sentiment analysis and employee feedback.Image Source: Shutterstock

BUILD A CASE FOR ROX

Institutions with the most significant decline are more likely to have a lesser focus on ROX. As measuring experience factors becomes increasingly common amongst larger banks, those not yet emphasizing ROX may fall further behind. Leveraging industry case studies on the impact of ROX, finding an internal C-Suite champion or hiring a ROX consultant to help facilitate the process are all strategies worth considering to gain support and traction in implementing new experience measurements.

The Road Map

It’s clear that experience matters in terms of differentiation and growth. Therefore, ROX measurement is a critical tool in helping banks determine the best path to creating banking experiences that will deliver what consumers want.

The first step would be to start with an analysis of what your institution is monitoring and the level of primary research on what your banking customers want from your brand. Developing a view of the ideal experience through a multi-faceted consumer engagement initiative, including ethnographic study, quantitative data and existing customer feedback will help banks understand where they have opportunities to improve. Leveraging this vision of the future, with clearly defined, measurable goals for a return on experience, will help bank executives get buy-in from their teams and leaders, helping them create a clear vision of the future for their bank.

About the author

Jean-Pierre Lacroix, President, SLD

Innovator, designer, strategist, futurist, transformer of brands for growth, Jean-Pierre Lacroix is President of Shikatani Lacroix Design (SLD). Jean-Pierre Lacroix is strongly committed to design innovation. In addition to pioneering the successful firm, Jean-Pierre is also Past President of The Association of Registered Graphic Designers of Ontario, Past President of DIAC (Design Industry Advisory Committee), board member of SEGD (Society of Environmental Graphic Designers), as well as former Director of the Packaging Association of Canada.

SLD is a founding member of the H2D Collective

The organization helps drive greater transformational value for retailers, banks and service-driven industries. The H2D Collective is a group of industry-leading experts and brands dedicated to putting humans at the center of your digital transformation. Their combined expertise provides a human-centric and agile approach that ensures technology helps your team deliver world-class customer experiences. Current members of the Collective represent leaders in their fields, namely Intel, Engageware, Diversified, Ath Power, Bridjr, OPTiFi and SLD.