Shikatani Lacroix Design (SLD) was invited to speak at the ebankIT Summit in Portugal on the future of seamless advice and its impact on customer loyalty in the banking sector. The presentation was based on a consumer study with a detailed comparison of the banking industry in North America and the EU/UK. It revealed nuanced regional differences in customer behavior, preferences, and the banking environment. These differences span across various aspects, including digital adoption, branch banking, customer expectations, and the regulatory landscape.

In addition, the study provides insights into the need, definition, and use of seamless banking in different markets. The comparison found unique approaches and preferences in these areas, highlighting how seamless banking is perceived and implemented differently. The study also sheds light on the importance of financial advice in banking and how it shapes customer loyalty. In this blog, we’ll go over the major findings of this study as a recap of the presentation.

Regional Differences

In North America, particularly in the United States, there is a definite trend toward digital and mobile banking. The study indicated that U.S. consumers had a strong preference for mobile banking apps, highlighting the region’s rapid digital development. In comparison, the EU and UK markets exhibit a more balanced approach, with digital banking increasing at a slower pace. Differences in client demographics, technology infrastructure, and cultural views regarding banking operations can all contribute to this diversity.

Understanding Seamless Banking

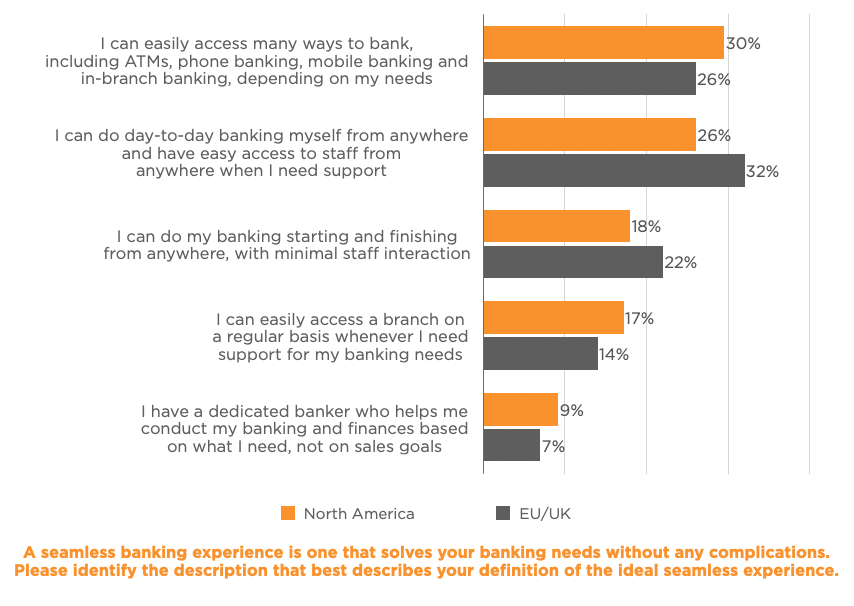

At its foundation, seamless banking is a quick and easy experience that meets the needs of the customer. It is about the seamless integration and interaction of multiple financial channels, both digital and physical. It guarantees that customers can manage their finances without interruption. A seamless banking experience is one that solves banking demands without hassles.

However, regional differences exist. In North America, seamless banking mostly refers to having quick access to all banking channels and expertise. Customers desire to conduct everyday banking independently while having staff assistance available. The emphasis in the EU and UK is on day-to-day banking support, implying a preference for banking solutions that integrate several banking modalities, such as ATMs, phone banking, mobile banking, and in-branch banking. In this regard, combining self-service and assisted banking experiences could be beneficial.

Image Source: SLD

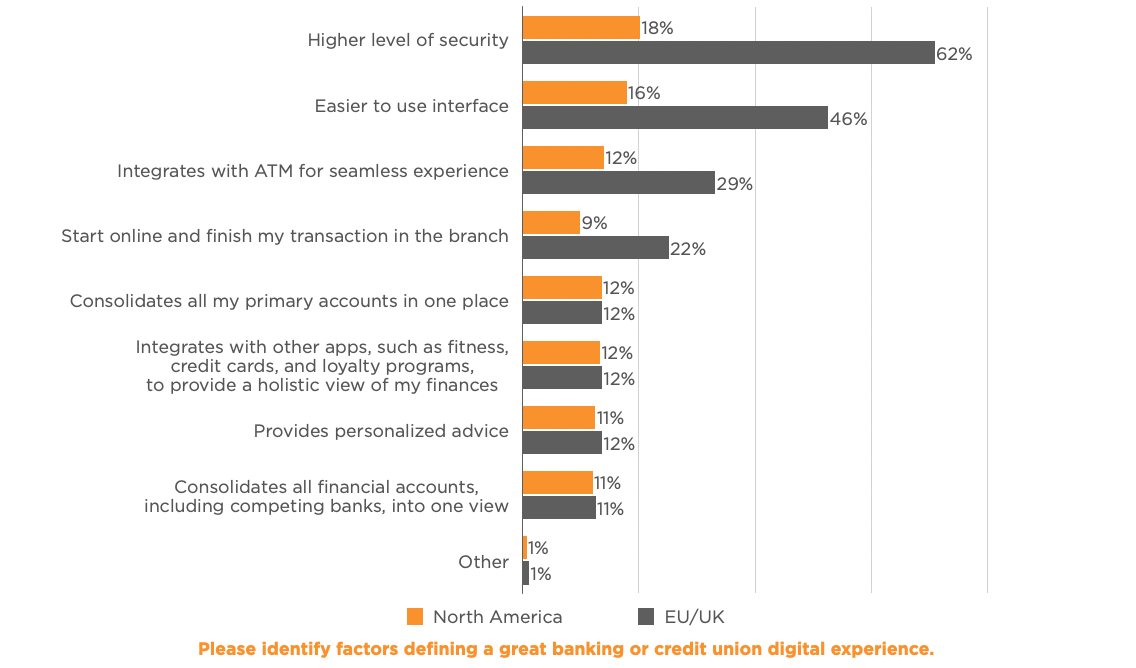

Use and Improvement of Banking Channels

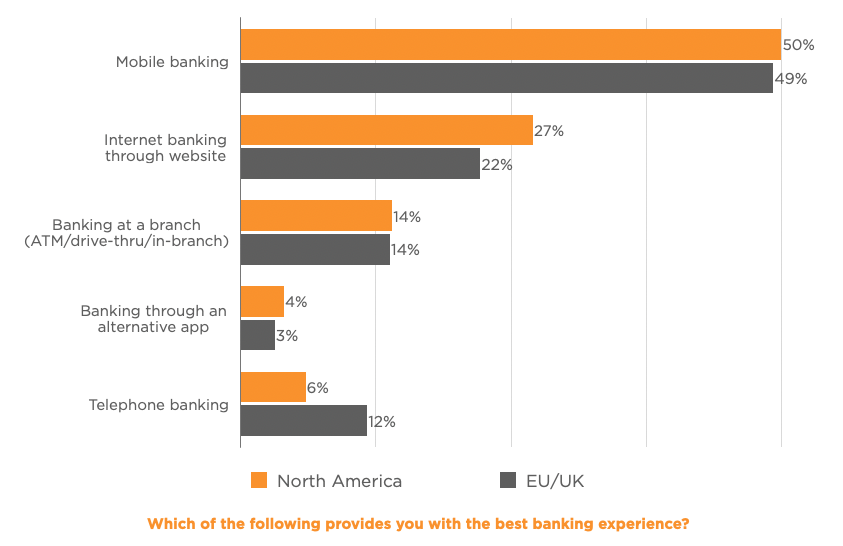

According to the study, the need for improvement in banking channels varies. For instance, internet banking requires minor improvement, while branch experience, particularly in Canada, needs to be significantly enhanced. Mobile banking is widely used in both locations. The EU and UK, on the other hand, scored higher for telephone banking and lower for internet banking. These findings suggest that preferences and degrees of comfort differ between banking channels. Security, followed by an easy-to-use interface, remains critical to delivering an outstanding digital banking experience. This is consistent with the broader trend of seamless banking, in which merging security and user experience (UX) is critical.

Image Source: SLD

Branch Banking and Digital Integration

Despite the digital shift, branch banking continues to serve an important role, with noticeable interruptions such as closures, relocations, and restorations. The study, however, showed no significant differences in branches between the Canadian and US marketplaces. Customers in Canada have fewer banking apps than their counterparts in the United States. This revealed a regional variance in the continent’s adoption and dependence on digital banking instruments.

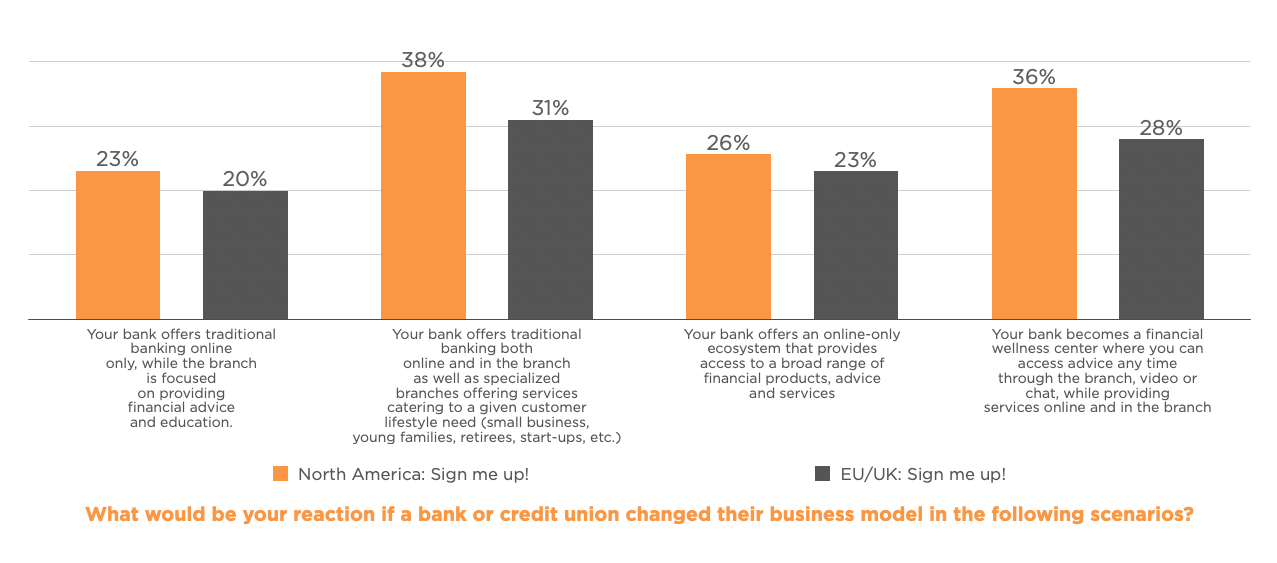

Customers in North America and the EU/UK expressed interest in branches that provide specialized services, such as convenient access to financial specialists and a greater selection of products and services. This indicates that branches must evolve beyond traditional banking.

Image Source: SLD

In addition, the role of physical branches in North America, particularly in the U.S., has shifted significantly toward tech-centric hubs. These branches are aimed at digitally sophisticated customers, with a greater emphasis on specialized services and customer involvement through technology. Despite the integration of digital tools into branches in the EU and UK, conventional branch structures endure. Personal advice and client service are prioritized in these places, reflecting a different approach to blending digital and traditional banking practices.

Branches are changing to provide services other than traditional banking. There is a trend toward offering a broad range of financial advice and education to certain customer segments, such as small enterprises, start-ups, young families, and retirees. This strategy suggests a shift toward more personalized and lifestyle-oriented financial services.

Customer Behaviors and Expectations

North Americans have a strong need for individualized, technologically enhanced banking services. This region’s customers seek more personalized products and services. This tendency is less visible in the EU and UK, where customers place a higher value on the reliability and integrity of their financial institutions. In comparison to North America’s service-oriented culture, the EU/UK is more relationship-focused.

Customers’ impressions of a bank’s ability to provide a seamless banking experience are shaped by branding. As a result of this perception, the brand needs to demonstrate dependability, knowledge, and customer-centricity. It is not only about transaction efficiency but also about the quality of interactions and whether the bank truly understands the demands of its customers.

The Link Between Financial Advice and Seamless Banking

There is a perceived disparity in satisfaction with financial advice across demographics and geographies. This variety emphasizes the need for banks to understand and cater to the varied advice needs of their broad customer base.

Financial advice is a crucial factor in customer satisfaction. There is a noticeable difference in satisfaction levels for financial advice across demographics and geographies. This variety highlights the importance of banks understanding and catering to the individual needs of their broad customer base.

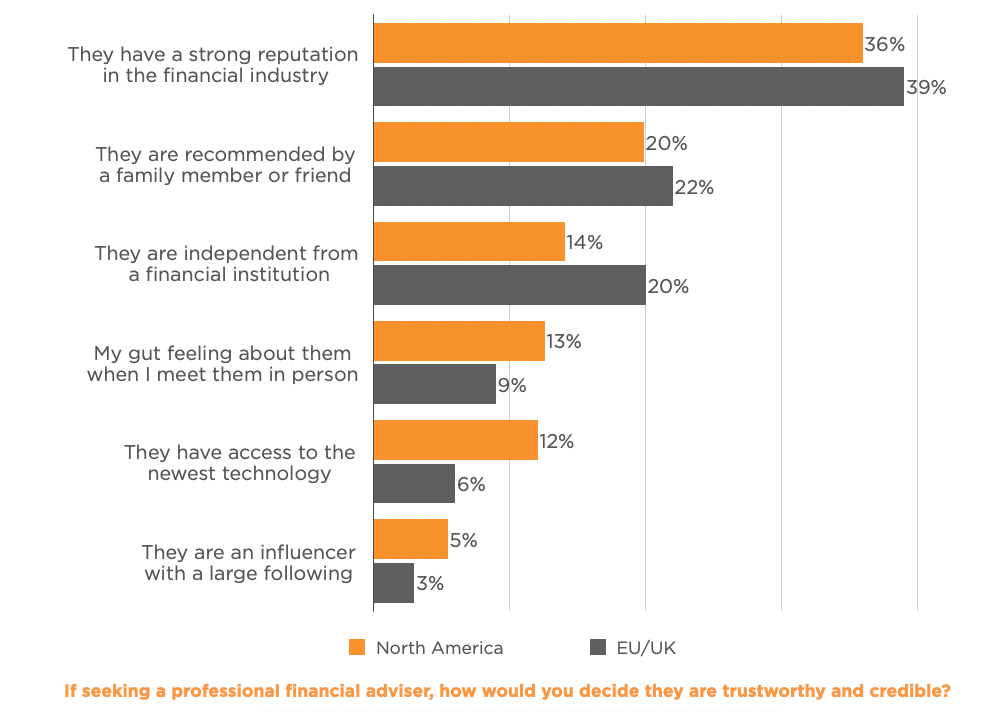

Customers place a high value on financial advice that is tailored to their specific circumstances and delivered by experts with extensive knowledge and trustworthiness. Access to a wide choice of non-commission-based solutions and advice is also important. Customers seek unbiased, all-inclusive financial advice.

Several factors influence financial advice credibility, including brand reputation, recommendations from family or friends, independence from financial institutions, and usage of cutting-edge technologies. These issues emphasize the complexities of trust in financial advice and the importance of institutions establishing reputations through many channels.

Image Source: SLD

Regulations and Security

In addition, the study emphasizes regional disparities in regulatory settings and security issues. North American banks, particularly those in the United States, must navigate a complicated and frequently fragmented regulatory structure. The EU/UK, on the other hand, is controlled by several frameworks, like the General Data Protection Regulation (GDPR), which emphasizes data protection and client privacy. This has an impact on how banks in various locations deal with security and compliance issues.

Innovation and Technological Adoption

The rate and nature of technological adoption in banking differ greatly across these regions as well. North American markets, particularly the United States, are frequently at the forefront of embracing new technology and developments. This is due to a highly competitive and diverse banking environment. The EU and UK markets, on the other hand, are inventive, but they tend to adopt new technology with caution, focusing on integration with established banking processes and systems.

Image Source: SLD

The Takeaway

The study sheds light on the varied banking landscapes of North America and the EU/UK. Understanding regional variances is critical for bankers and stakeholders, who must properly customize their strategy for each market. The report emphasizes the significance of understanding regional differences in client preferences, digital adoption, regulatory settings, and the balance between digital and traditional banking. As the banking industry evolves, these insights will be critical in defining future strategies and services to meet the specific needs of each region.

While the core concept of seamless banking — a hassle-free, integrated banking experience — is consistent, its interpretation and implementation differ significantly between North America and the EU/UK. North America favors digital independence and ease of access, whereas the EU and UK strike a balance between digital convenience and traditional financial assistance.

The research also reaffirmed the significance of tailored and trustworthy financial advice. It boosts client retention, loyalty, and brand trust. Banks will likely see increased client loyalty and gain a competitive advantage by including accessible, tailored, and trustworthy financial advice in their service offerings. Our findings highlight the increasing role of financial advice in banking and its impact on building long-term customer relationships.