About half of Gen Z are now over 18 and are making adult financial decisions. As banks and other financial institutions look to the future, what does this diverse young generation want? In this blog, we explore emerging trends in banking preference and behavior, the driving forces behind these changes, and what banks can do to appeal to younger consumers.

FINANCIAL OUTLOOK

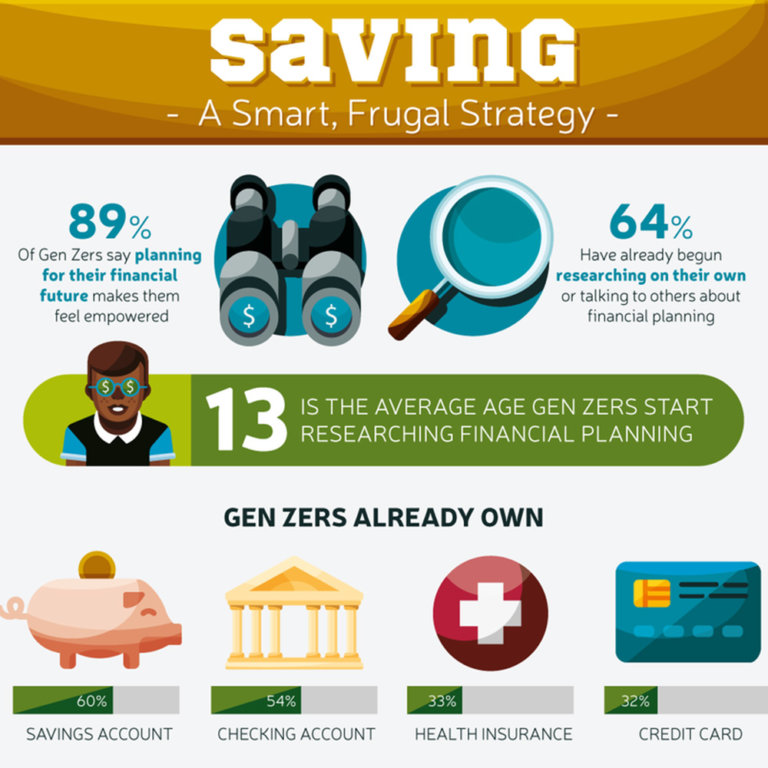

Gen Z have inherited a sense of pragmatism from their Gen X parents that differentiates them from Millennials. Gen Z’s perspective on finances is strongly influenced by their parents’ struggle to pay off student loans, Millennials’ homeownership challenges and rising income inequality. Given their elders’ experiences, it’s not hard to understand why Gen Z is taking a prudent approach to money.

KEY DRIVERS OF BANKING BEHAVIOUR IN GEN Z

When we look at the ways in which Gen Z wants to manage their money, there are five key factors influencing them: a digital-first perspective, self-education through social media, pragmatism, parental influence and an activist mindset. Let’s dive into these five driving forces.

1. DIGITAL-ONLY MINDSET

When grandparents send a cheque in a birthday card, will Gen Z kids know what they are? Less than half have written a cheque and many never will. Thinking of Gen Z as digital-first is helpful but understanding that 37 percent are looking for digital-only should put this in perspective. Here’s what that means for financial brands:

- Digital experiences need to be best-in-class to meet Gen Z expectations. That includes entertainment, education, seamless omni-channel and exceptional user experience. Anything less is not going to impress. Adding bells and whistles to an average system is not going to meet Gen Z’s standards.

- Connection is key. Although they will primarily utilize mobile banking services, Gen Z also visits physical branches. Currently, few banks offer a truly seamless experience that connects their physical touchpoints to the digital experience. This is kind of next-level connectivity matters to Gen Z – they don’t experience digital as separate from the physical world and will engage with brands that reflect that experience.

- Be future-ready. Cryptocurrency and other alternative payment methods will disrupt traditional banks if they are not paying close attention and ready to move.

2. SOCIAL MEDIA SELF EDUCATION

Gen Z loves video content and content creators. Many seek financial advice online, even while they recognize social media is a highly unreliable source. With 23 percent saying educational resources are a problem when it comes to financial literacy, this currently unmet need is being filled by influencers, some of whom offer excellent advice, other with dubious credentials. Many banks are creating video content but it’s quite corporate in tone. Banks need to learn from the kind of video content Gen Z is watching. Here are some key takeaways:

- Banks need to watch influencers such as Roaring Kitty, Andrej Jikh, Tori Dunlap or Taylor Price to understand the style and approach that Gen Z finds engaging.

- While regulators are attempting to control financial advice on social media due to its unreliability, there is little reason to believe they will succeed. Banks and other financial institutions can help guide consumers to better sources through sharing quality content on their platforms, reviewing influencers in “Top 10” lists and creating similar content and/or endorsing specific creators. Many financial influencers have a deep and complex grasp of financial management and offer excellent advice. The challenge for the consumer is in knowing who can be trusted – banks could help with that.

3. PRAGMATISM

Even before the pandemic, market analysts were using the term “prudent” to describe certain trends amongst Gen Z, including less alcohol consumption, less sexual activity and less frivolous spending. There are multiple factors contributing to this overarching attitude: more screen time, a compressed middle class and a rise in mental health issues. Here are the implications for financial brands:

- Gen Z is substantially more debt-averse than previous generations. To avoid student debt, many will attend an alternate post-secondary school rather than their first choice, live with their parents longer and choose career paths based on immediate and future financial incentives. They hold fewer credit cards and prefer to use debit. Financial institutions should consider providing low-interest student loans and bank products to give young people financial support when they need it most. Given how anxious Gen Z is about money, this is a powerful way for brands to build trust.

- Gen Z are straight shooters who don’t like fine print or sales pitches. Banks need to take transparency on as a critical mission. If Gen Z thinks they’ve been duped, they will share that experience widely on their social networks. Given how much they credit peer reviews, brands need to get ahead by removing choice architecture that favors the brand over the consumer and being upfront about… well, everything.

- Gen Z is not lured by a perfectly filtered edit. Their strong preference for less heavy-handed design can be seen in platforms such as TikTok and Discord. Superior function comes first and, while the design is still important, Gen Z prefers simplicity, authenticity and even a little messiness to a perfect, contrived approach.

4. PARENTAL INFLUENCE

Raised by Gen X parents, Gen Z enjoys close familial relationships that widely favor open dialogue over discipline. As a result, not only do their parents influence their choices but Gen Z wields considerable influence over their parents.

- Multi-generational services that allow discounts, shared rewards, shared saving for specific goals and bundling are highly relevant, as Gen Z enjoys parental financial support well into their 20’s.

- Gen Z are very likely to start their banking experience with the same financial institution as their parents. However, as they become adults they are likely to explore alternative payment and financial services that cost less and offer rewards – and they are likely to influence their parents to sign up for these services as well.

- While Millennials were “bubble-wrapped” by “helicopter parents,” Gen Z has enjoyed a more laissez-faire style of parenting. Most recently, they’ve had to deal with major personal disruptions as the pandemic threw their educations and first jobs into turmoil, with many losing a year from their planned timelines. This sober and anxious demographic will likely follow in their Gen X parents’ footsteps when it comes to life timeline, focusing more on a career path, stable jobs and financial security than social fun, travel and entrepreneurship. Financial products for this generation should consider a more fiscally conservative life journey.

5. ACTIVIST MINDSET

We are continually told that Gen Z is the most diverse and best-educated generation ever, but we talk less often about what that means in concrete terms. When it comes to financial brands, here are some key considerations:

- Climate change is not just a liberal value when it comes to younger generations. Conservative Gen Z’ers also want climate action. Banks need to consider the big picture in terms of investments and have a transparent plan for reducing their carbon footprint.

- Compared to other industries, leaders in finance are more likely to be white, male, heterosexual and cisgender. To create a pipeline of new financial leaders who better represent the customers they serve, financial brands need to ensure diverse students see themselves in the industry, have educational pipelines that lead them to finance as well as the resources to do so, and are given growth opportunities within the organization.

- Open attitudes among Gen Z are most visible in their willingness to share personal stories online. While this openness may feel positively shameless to older generations, to Gen Z that’s precisely the point. They want to have frank conversations about matters such as money without shame or judgement. Banks are not viewed as transparent and honest. A new approach that puts all the cards on the table may seem like a shock, but it will be necessary if financial brands want Gen Z to stay with them as they get older.

One Final Note: Gen Z, like any other generation, is a diverse group of individuals who have unique perspectives and needs. These drivers of behavior are starting points that will be largely relevant to the majority of this generation. From here, creating personas that reflect the specific needs of your Gen Z customers will help financial brands deliver on the kind of personal experience they want.